Somewhere right now, a freelancer is standing in a bank queue with a folder of documents, two references, and a passport photo, trying to open a dollar account. And somewhere else, another freelancer just opened a USD account online from her phone in under ten minutes, got US account details in her own name, and sent them to her client before lunch.

Same goal. Wildly different experience. The difference is knowing that in 2026, you no longer need a traditional bank, a US address, or a plane ticket to own a dollar account.

This guide covers how to open a USD account online from anywhere in Africa, the Middle East, or Europe, what you can do with it, what to check before choosing a provider, and how to start receiving dollar payments the same week.

What Is a Virtual USD Account?

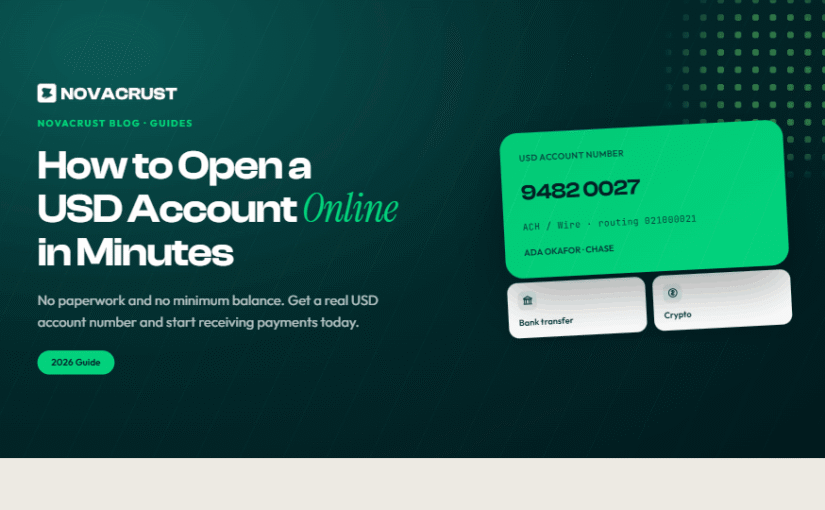

A virtual USD account is a dollar account you open and manage entirely online. It comes with real US account details in your name, an account number, and a routing number, with support for ACH, wire, and RTP transfers. To anyone paying you, it works exactly like a US bank account. To you, it is an app on your phone.

That single feature unlocks a lot. Clients and employers can pay you the way they pay anyone in America. Freelance platforms can deposit your earnings directly. And your money sits in USD, protected from local currency swings, until you decide to convert.

Check out this simple guide on ACH vs Wire vs SWIFT: Which Should You Use to Get Paid From Abroad?

Who Needs a Dollar Account?

If any of these sound like you, a USD account is not optional; it is infrastructure:

- Freelancers and remote workers. You earn from clients in the US, UK, or Europe and need a clean way to receive dollar payments without losing a chunk to middlemen. A USD account for freelancers means you invoice in dollars and keep dollars.

- Creators. YouTube, sponsorships, digital product sales. Platform payouts land far more easily in a US account than through legacy transfer chains.

- Savers. When your local currency is volatile, holding part of your income in a dollar account is the simplest hedge available. You convert what you need when the rate favors you.

- Small businesses and SMEs. Paying international suppliers and receiving from international customers both get easier when you operate a dollar balance.

Read: How Freelancers in Africa Receive International Payments Easily

How to Open a USD Account Online with Novacrust

Here is the entire process, and why it answers the classic search: how to open a dollar account without visiting a bank.

Step 1: Sign up and verify your identity

Sign up on Novacrust, create your account, and complete identity verification with a valid government ID or passport. No branch visit, no references, no minimum deposit. Verification typically takes minutes, not days, and works across most countries in Africa and the wider EMEA region. This is also the answer to another high-intent search: a USD account without a US address. You do not need one. The account is in your name, at your address, wherever you live.

Step 2: Get your US account details

Once verified, you get your account number and routing number with ACH, wire, and RTP support. These are the same details any American would hand over to get paid.

Step 3: Start receiving dollar payments

Share your details with clients and employers, or plug them into platforms like Upwork, Fiverr, Toptal, Andela, Deel, Gusto, Rippling, and YouTube. If you have ever searched for a USD account to receive Upwork payments, this is the setup: withdraw from the platform straight into your own dollar account.

Step 4: Hold, spend, convert, or send

Your dollars are yours to manage. Hold them as savings. Spend them with a virtual USD card on subscriptions, tools, and ads. Convert to your local currency at a competitive rate. Or send money to a local bank account or mobile money wallet, yours or anyone else’s.

What to Check Before Choosing a USD Account Provider

Not every dollar account is built the same. Compare providers on these five points:

- Real US account details with ACH and wire support. Some apps only give you an internal wallet. You want an account number and routing number that any US employer can pay, which also covers the search dollar account with ACH and wire support.

- Receiving fees. The best providers charge little or nothing to receive ACH payments. Wire fees vary, so check both.

- Conversion rates. The exchange rate is the hidden fee. Compare what actually lands in your local currency, not the advertised rate.

- Withdrawal options. Look for direct withdrawal to local banks and mobile money in your market, whether that is naira, cedis, shillings, rand, or dirhams.

- Everything in one app. A USD account gets far more useful when it lives beside a virtual card, crypto conversion, and local transfers, so your money moves without app hopping. That is the Novacrust ecosystem in one sentence.

Virtual USD Account vs Traditional Foreign Currency Account

| Traditional bank dollar account | Virtual USD account (Novacrust) | |

|---|---|---|

| Opening time | Days to weeks, branch visit | Minutes, fully online |

| Requirements | References, paperwork, and sometimes a minimum balance | Valid ID |

| Receiving a US wire | $60 to $100 in combined fees | Low, transparent fees |

| ACH support | Rare | Yes, standard |

| Withdrawal | Branch processes | Local bank or mobile money from the app |

| Best for | Large occasional transfers | Regular international income |

For most remote workers in Africa and EMEA, the comparison ends quickly. The best USD account for remote workers in Africa is the one that opens in minutes, receives ACH for little or nothing, and cashes out locally on your schedule.

Smart Ways to Use Your Dollar Account

- Split your income the moment it lands. A common freelancer formula: convert what you need for the month, hold the rest in USD as savings, and keep a small buffer on your virtual card for subscriptions.

- Time your conversions. Rates move. Because your money sits in dollars by default, you convert on the days that favor you, not the day your payment happens to arrive.

- Keep your payment history clean. Regular international income into an account in your own name builds a paper trail that helps with visa applications, apartment hunting, and credit.

Read this simple guide on Money Management for Remote Workers and Digital Nomads: The Complete 2026 Guide

Frequently Asked Questions

Can I open a USD account online without a US address?

Yes. Novacrust gives you US account details in your own name using your local identity documents. No US address, residency, or SSN required.

How long does it take to open a dollar account online?

Minutes. Sign up, verify your ID, and receive your account details, typically the same day.

Is a virtual USD account safe?

Reputable providers use identity verification, encryption, and regulated banking partners. Your account details work like standard US banking rails via ACH and wire.

Can I withdraw from my USD account to mobile money?

Yes, in supported markets, you can convert and withdraw funds directly to local banks or mobile money wallets through the app.

Does a USD account work for platform payouts?

Yes. Upwork, Fiverr, Toptal, Deel, YouTube, and many more can pay directly into your US account details.

The Bottom Line

A dollar account used to be a privilege that required the right passport or the patience for bank bureaucracy. Now it is a ten-minute setup. If you earn internationally, save seriously, or run a business across borders, opening a USD account online is the single upgrade that makes everything else about your finances simpler.

Open your Novacrust USD account in minutes and get US account details in your own name. No US address required.