The US has more than 4,000 chartered banks. Almost none of them will open an account for someone with no Social Security number and no US address. That single requirement is why so many freelancers, business owners, and diaspora workers outside the US spend hours filling out bank applications only to get rejected at the last step.

If you get paid in dollars, or want to, understanding how the US banking system actually works, and where it shuts non-residents out, saves you that wasted time. Here is what the system looks like from outside, and the faster way in.

The Three Accounts Everyone Means When They Say “US Bank Account”

Checking accounts. Built for daily use: receiving deposits, paying bills, spending with a debit card. This is the account most freelancers actually need.

Savings accounts. Built to hold money and earn a small amount of interest. Most banks pair a savings account with a checking account, not instead of one.

Credit unions. Member-owned instead of shareholder-owned, often with lower fees, but membership usually requires a US address, employer, or local affiliation, which rules most non-residents out immediately.

What Actually Blocks Non-Residents

Four things stop most applications before they start:

A Social Security Number or ITIN. Chase, Bank of America, and Wells Fargo all ask for one on the standard application. Without it, some branches will still open an account in person; most online applications reject you automatically.

A US address. Banks mail debit cards, statements, and tax forms. No US address usually means no account, even if every other requirement is met.

An in-person visit. Many banks still require you to walk into a branch with a physical ID to finish verification, which is not realistic if you live in Lagos, Nairobi, or Accra.

Minimum deposits and monthly fees. Traditional accounts often carry $10 to $25 monthly fees unless you maintain a minimum balance, on top of the paperwork.

Big Banks vs Online Banks vs Neobanks

Big banks (Chase, Bank of America, Wells Fargo) have the most name recognition and the strictest requirements for non-residents. A handful of branches make exceptions with extra documentation, but this varies by location and isn’t something you can rely on.

Online-only banks loosen some requirements but most still ask for an SSN or ITIN, since they are still bound by the same federal rules as physical banks.

Fintech platforms with USD Accounts work differently. Instead of opening a bank account in the traditional sense, you get real US account and routing numbers issued through a banking partner, without needing an SSN, ITIN, or US address yourself. This is the category Novacrust’s USD Account falls into.

The Vocabulary Worth Knowing

Three terms come up constantly once money starts moving into and out of a US account:

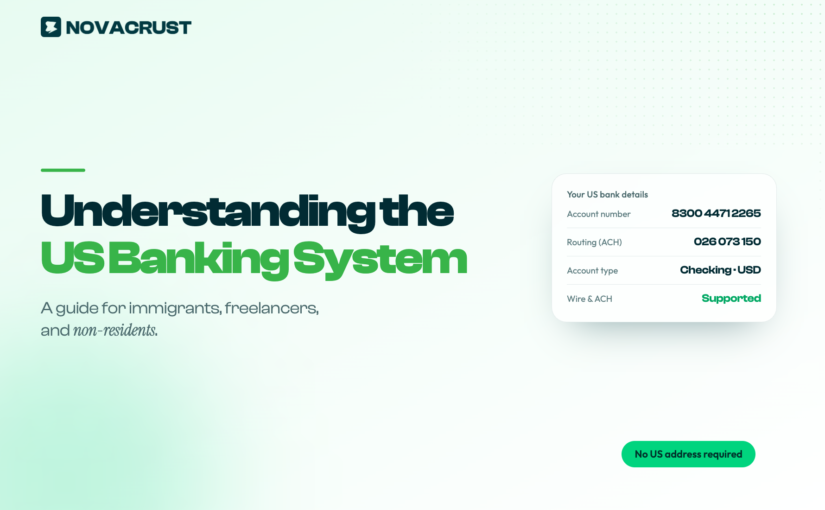

Routing number. Identifies the bank. Every US account has one.

Account number. Identifies you specifically within that bank.

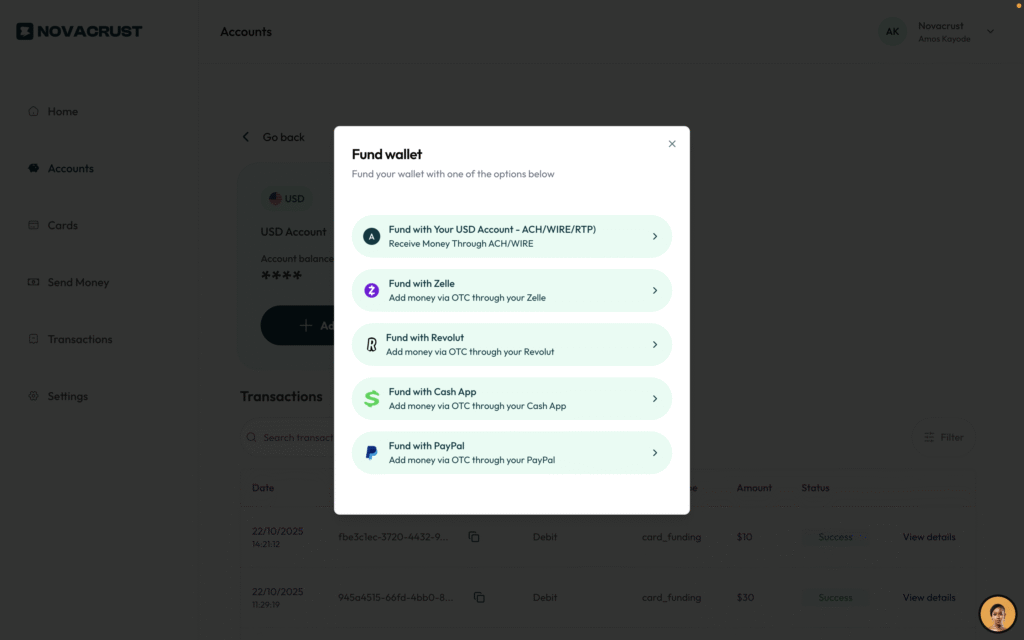

ACH, wire, and SWIFT. The three ways money actually moves. ACH is the standard, low-cost domestic transfer method. Wires move faster and cost more. SWIFT handles international transfers between banks in different countries.

Read: ACH vs Wire vs SWIFT: Which Should You Use to Get Paid From Abroad?

The Faster Way In: A USD Account Built for Non-Residents

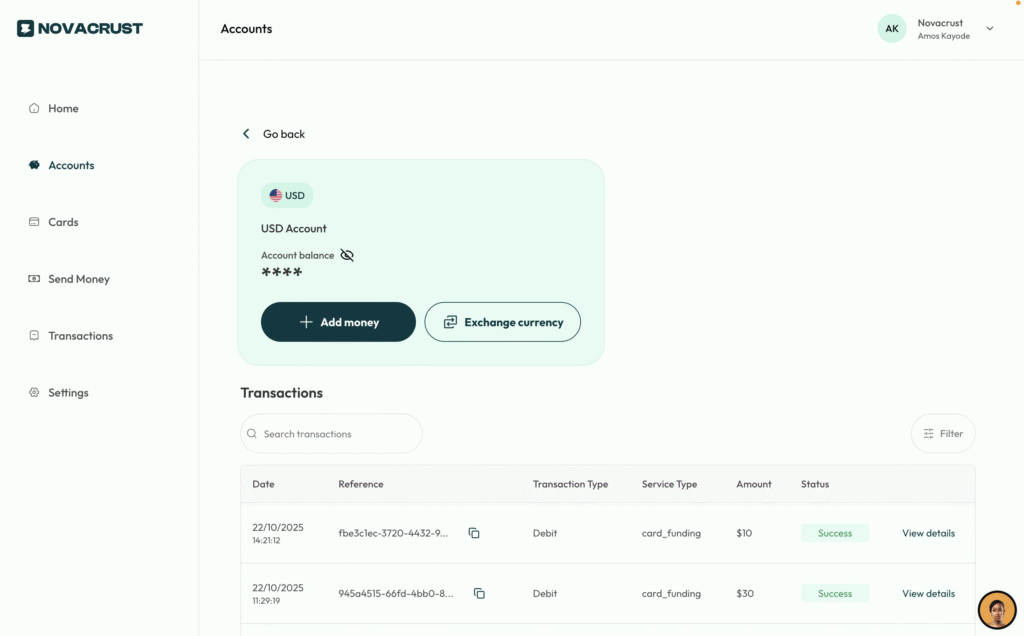

You do not need to become a customer of a traditional US bank to receive dollars like one. With Novacrust, your USD Account gives you a real US account and routing number in your name, so clients on Upwork, Fiverr, or direct contracts can pay you exactly like they would pay someone based in the US.

No SSN. No US address. No branch visit. You open it from your phone, and it works alongside your crypto wallet, virtual card, and transfers to 50+ countries in the same account.

Read: How to Open a USD Account Online in Minutes

Frequently Asked Questions

Can a non-US resident open a US bank account? Rarely through a traditional bank without an SSN, ITIN, or US address. Fintech platforms offering USD Accounts solve this without requiring US residency.

Do I need a Social Security Number to receive USD payments? No. A USD Account from Novacrust gives you US account and routing numbers without an SSN.

What’s the difference between a checking account and a USD Account? A checking account is issued directly by a US bank to US residents. A USD Account is issued through a fintech platform’s banking partner and works the same way for receiving and sending dollars, without the residency requirements.

Can I withdraw or convert the dollars I receive? Yes. With Novacrust, dollars in your USD Account convert to your local currency at a competitive rate, or move on as crypto, whenever you choose.

Is a USD Account the same as a domiciliary account? No. A domiciliary account is held at a bank in your own country and usually still requires branch visits. A USD Account gives you a real US account number directly.

The Bottom Line

The US banking system was not built with non-residents in mind. You don’t need to fight it. Get the parts that matter: a real US account and routing number, without the SSN, the address, or the branch visit.

CTA: Get Started. It’s Free. Open your Novacrust USD Account and get paid in dollars from anywhere.